MTN launched a rollover BEE vehicle to replace the existing Zakhele vehicle called MTN Zakhele Futhi (“Futhi”). 3 options are available to subscribe to this new scheme and SimpleAlpha comments on those choices

Option 1 – Cash out of Zakhele

Trading at the current share price of R65 per Zakhele share (original cost of R20p/s) results in an effective annual return of 22%.

An alternative solution is contacting a Nedbank branch and elect to receive cash upon expiry of Zakhele by 21 October 2016.

Option 2 – Convert MTN Zakhele into MTN directly.

If, based on the assumptions above, the terminal Zakhele is valued at R65p/s and further assuming MTN share price of R121p/s on 21 October 2016, a conversion ratio of 1.86 Zakhele shares to 1 MTN share is observed (less if other unwinding costs are incurred)

Option 3 – Convert into MTN Futhi

Similar to option 2 the cash value of your Zakhele investment is rolled into the Futhi scheme. Again assuming R65p/s value for Zakhele results in 3.25 Futhi shares at R20p/s. There is a 3 year lock in for all shareholders followed by a further 5 years where BEE participants can trade amongst themselves, after which free trade commences.

The Futhi prospectus breaks down individual components of the deal based on an MTN share price of R128.5 as follows:

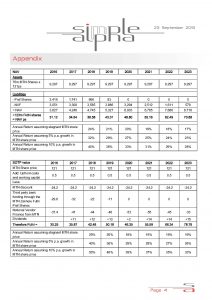

| Total (R million) | Per MTN Share (R) | % | |

| Equity from MTN Zakhele Futhi Public Offer and MTN Zakhele Re-investment Offer | 2,468.30 | 32.12 | 25% |

| Upfront costs and working capital | (39.4) | (0.51) | 0% |

| MTN discount | 1,974.60 | 25.7 | 20% |

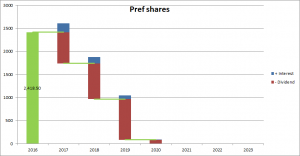

| Third party bank funding through the MTN Zakhele Futhi Pref Shares | 2,418.50 | 31.48 | 24% |

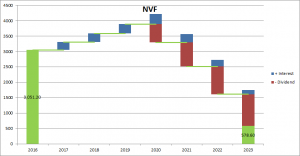

| Notional Vendor Finance from MTN | 3,051.20 | 39.71 | 31% |

| Total | 9,873.20 | 128.5 | 100% |

If the MTN share price encroaches into R114p/s territory by October 2016 and assuming MTN Discount, Pref Share and NVF funding remain the same, the Equity value of R32.12 is depreciated to the R20 offer price reducing Futhi’s attractive initial value discount.The key variables that will ultimately drive Futhi’s success is MTN’s share price, dividends received by Futhi from MTN and the debt repayment profiles.

Dividend growth rates claimed by MTN range from 5% to 15%. MTN have lagged behind in infrastructure spend and are beset by regulatory issues in Nigeria and Iran and cash flow restrictions may place the dividend growth rates closer to the 5% mark.

| Actual DPS |

Grown @5% |

||||||||

| 2016 | 2017 | 2018 | 2019 | 2020 | 2021 | 2022 | 2023 | 2024 | |

| Dividend per share | 10.8 | 11.3 | 11.9 | 12.5 | 13.1 | 13.8 | 14.5 | 15.2 | 16.0 |

| To Futhi (76m shares) R’m | 830 | 871 | 915 | 961 | 1,009 | 1,059 | 1,112 | 1,168 | 1,226 |

Dividends are first allocated to repay the pref shares and thereafter used to repay MTN Notional Vendor Finance loan. The calculations indicate a remaining NVF balance at the end of 8 years and thus 1 Futhi ≠ 1 MTN. The model is heavily reliant on MTN growing its dividend payments by a modest 5%, although there is a likelihood of dividend suspension if MTN hits cash flow crisis.

2 cursory methods were used to value Futhi over the term:

- – A simplified NAV taking Futhi’s assets (76m shares in MTN) less its NVF and Pref liabilities divided by the 123m shares Futhi will issue. Futhi’s only asset is shares in MTN and is particularly sensitive to movements in that price. We assumed 3 scenarios, a stagnant MTN share price, a 5% p.a. growth in MTN share price and a 10% p.a. growth in MTN share price. See appendix.

- – A sum of the parts (SOTP) value method was also used to corroborate the NAV. Here the deals’ individual components, as outlined by the prospectus, are extrapolated over the term. The calculated residual value is deemed to be Futhi’s intrinsic worth. MTN dividends are assumed to be applied to reducing pref share liability first and thereafter to the NVF. See appendix.

Both models reveal compounded annual growth rates in excess of inflation with terminal Futhi valuations of between R70 and R78 per share.

A new management team is in place but their effects will be felt over the long-term.The prospectus states that a R1 move in MTN is estimated at increasing/decreasing Futhi initial offer by 62cents. In percentage terms 1% MTN move = 3.75% Futhi move.

Despite a lack of dividends in Zakhele, illiquidity and trade restrictions (likely to persist in Futhi) investors have yielded 22% annualised due to the funding mechanisms. Futhi continues on a similar approach and an upward MTN share price will have a multiplier effect in Futhi.

An investor should seek the skills of a financial adviser who has dedicated their career to helping others reach their financial goals. Independent financial advisers (retail IFA’s) and asset consultants (Institutional investment advisors) know what information is relevant to developing a financial roadmap for their client and can separate themselves emotionally from making decisions on the most appropriate route to take. They would consider the clients risk tolerance, the appropriateness of investment style and diversification before suggesting a solution.

![]() Disclaimer: SimpleAlpha is not licensed to provide financial advice and while our authors may be professionals in their respective fields, we do not make ourselves out to be experts in the matter of financial planning or the giving of financial advice.

Disclaimer: SimpleAlpha is not licensed to provide financial advice and while our authors may be professionals in their respective fields, we do not make ourselves out to be experts in the matter of financial planning or the giving of financial advice.

The information herein is intended to promote discussion and is purely for information purposes only. This includes but is not limited to the concepts explained, the thoughts of our writers, as well as our opinions and forecasts, whether implied or not, and is certainly not intended to be construed as financial advice.

Appendix: